Trends That Rise and Fall

Startups innovate, thrive, or vanish swiftly. Success depends on adapting to challenges and shifting markets.

The startup world is a dynamic one, constantly buzzing with innovation and new ideas. Some rise reaching the unicorn label, only to fade into obscurity just as quickly, while others leave a lasting impact. Trends often emerge in response to market demands, technological advancements, or shifts in consumer behavior.

The startup landscape is characterized by a constant cycle of innovation, experimentation, and adaptation. What captures widespread attention and investment today may not necessarily endure in the long run. Some trends become foundational pillars of industries, while others fade into obscurity due to scalability challenges, regulatory hurdles, or shifts in market dynamics.

Cloud Kitchens

The concept of cloud kitchens, pioneered in 2015 by the Indian company "Rebel Food," represents a paradigm shift in the food service industry. Operating without physical dine-in spaces, these establishments rely on centralized kitchens to efficiently fulfill delivery and takeout orders through various online platforms. Within the cloud kitchen players, there are two primary models: the one that only rents spaces to tenants and one that also manages the brands’ operations as well. In this article, our focus lies on the rental model of cloud kitchens, where the emphasis is placed on providing space and basic amenities.

The rise of cloud kitchens owes much of its momentum to the seismic shifts induced by the COVID-19 pandemic within the food and beverage industry. Lockdowns, social distancing measures, and consumer reluctance to dine out created an unprecedented surge in demand for food delivery services.

Edison Trends' 2021 survey revealed a growing trend of increased reliance on food delivery services in various regions. Similarly, A Google, Temasek, and Bain study revealed a dramatic shift in Southeast Asian consumer behavior during the pandemic, with online food delivery services’ GMV skyrocketing by 150% from USD 6 billion in 2020 to USD 15 billion in 2021.

Meanwhile the GMV growth from 2019 to 2020 was only 15%, from USD 5.2 billion to USD 6 billion. These findings underscored a worldwide behavioral shift towards the convenience and popularity of food delivery services during the COVID-19 pandemic.

CloudKitchens, a trailblazer in the US cloud kitchen sector, garnered substantial success, securing an impressive USD 1.3 billion in funding within its first five years of operation (2016-2021) and attaining a valuation of USD 15 billion. However, post-pandemic, the company has encountered a downturn. Forced closures of operational sites, such as those in New York and Tennessee, and staff reductions became necessary due to low occupancy, with only 50% of warehouses occupied by Q1 2023.

This trend extends beyond CloudKitchens, as evidenced by the closure of all US-based Kitchen United kiosks in Kroger Supermarkets. While in Southeast Asia, Grabkitchen has also closed its operation in Indonesia since 19 December 2022. These examples are only a fragment of declining theme in the industry.

Several factors that contribute to the downfall of rental-modeled cloud kitchens are:

Return to old consumer habits post-pandemic. As lockdowns eased and dining options reopened, consumers reverted to familiar habits of dining out, reducing the sustained demand for delivery-only meals that initially fueled the growth of these kitchens.

Hindered economies of scale as attracting diverse range of brands has been challenging. This stagnation in brand scaling is translated into vacant kitchen spaces, suggesting that the rental model is economically unviable, with operating costs, including rent, utilities, and maintenance expenses remained relatively high.

NFTs

Non-Fungible Tokens (NFTs) represent distinct digital assets with authenticated ownership through blockchain technology, typically encompassing digital art or collectibles. While the concept of digital assets dates back to 2014, their widespread adoption was materialized in 2021, primarily driven by social phenomena.

The surge in popularity was first catalyzed by the notable transaction involving an American digital artist, Beeple's "Everydays — The First 5000 Days," auctioned at Christie's for a staggering USD 69 million. This was further propelled by the active involvement of celebrities and renowned brands such as Adidas, Gucci, Hot Wheels, Coca-Cola, and Taco bell, transforming NFTs into a significant element of contemporary pop culture.

List of Popular NFTs Series

The Merge

Highest Price : USD 91.8 million

Transaction Date : Dec 2021

SXEverydays: The First 5000 Days

Highest Price : USD 69.3 million

Transaction Date : March 2021

CryptoPunks #5822

Highest Price : USD 23.7 million

Transaction Date : February 2022

TPunks #3442

Highest Price : USD 10.5 million

Transaction Date : August 2021

Bored Apple Yacht Club #8817

Highest Price : USD 3.4 million

Transaction Date : October 2021

Mutant Apple Yacht Club #4849

Highest Price : USD 1.1 million

Transaction Date : August 202

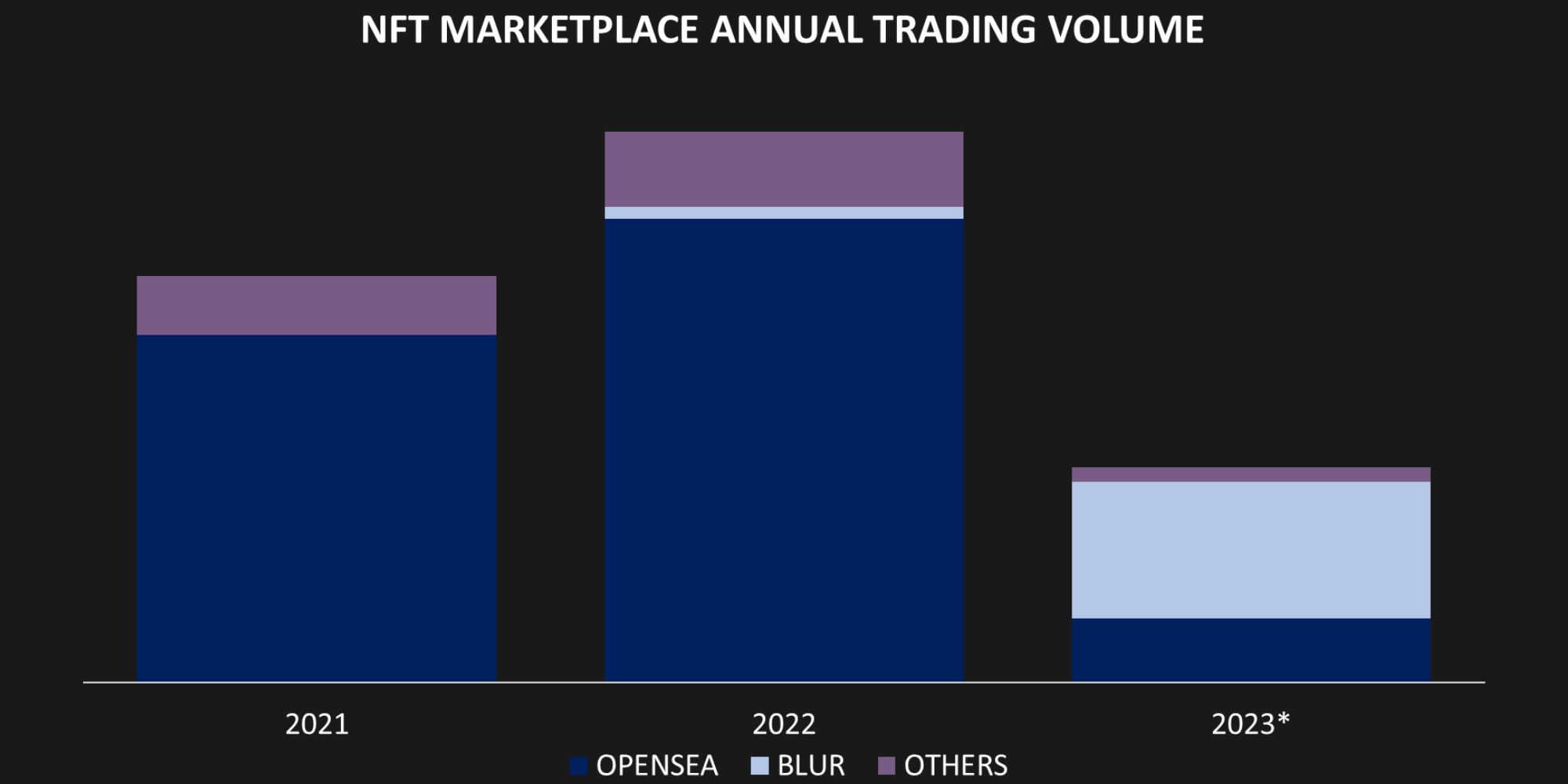

The rapid surge of NFT transactions primarily occurred in dedicated marketplaces, notably Opensea, a US-based startup that emerged as the market leader in 2021. Attracting substantial investments totaling USD 427 million, Opensea achieved a valuation of USD 13.3 billion after a USD 300 million Series C funding in January 2022 by Web3-focused investor Paradigm and growth-stage investor Coatue.

However, recent challenges led to significant workforce reductions, with 50% of total staffs being laid off in 2023

OpenSea is not alone in facing the decline; the entire NFT industry has witnessed a significant 61% decrease within just one year. Transaction values, which stood at USD 23.3 billion in 2022, have dwindled to a mere USD 9.1 billion in 2023.

Several factors that contribute to this downturn:

Unclear Value Proposition – No Copyright. Despite the potential of owning and interacting with narrative experiences, many users struggle to discern the concrete value proposition of NFTs. Ambiguities surrounding ownership rights, often subject to varying terms from one NFT to another, contribute to user skepticism and hesitation. The "right-clicker" argument, asserting that NFTs can be easily copied or screenshot, further adds to these uncertainties.

Low Adoption Rate. NFTs encounter barriers to widespread adoption, given their newness and the intricate blockchain technology behind them. The resulting lack of public awareness and understanding poses challenges for integrating NFTs into everyday transactions and activities.

Brand Aggregator

Brand aggregators have emerged as a significant force in the e-commerce ecosystem, revolutionizing the landscape of online businesses. These entities specialize in acquiring, consolidating, and scaling up a multitude of direct-to-consumer (DTC) brands. The core strategy of brand aggregators involves identifying successful and promising e-commerce brands and offering them an exit opportunity. By pooling these brands under their umbrella, aggregators leverage economies of scale, operational efficiencies, marketing expertise, and access to capital.

The growth of e-commerce, notably accelerated by the COVID-19 pandemic, has propelled the meteoric rise of brand aggregators. In 2020 alone, global e-commerce sales surged by 24.1% to reach USD 4.29 trillion. This unprecedented growth created a fertile ground for individual entrepreneurs. As these brands flourished, brand aggregators such as Thrasio, Perch, and others capitalized on this trend.

Thrasio, once a prominent brand aggregator specializing in acquiring top-performing brands in Amazon, now finds itself in financial distress. Despite securing a significant USD 3.4 billion investment from major players such as JP Morgan and Goldman Sachs between 2020 and 2022, the company is reportedly contemplating potential bankruptcy as of September 2023. Thrasio is not the only player struggling in the brand aggregators space. On the other side of the globe, Hypefast, an Indonesian fashion brand aggregator, is grappling with revenue issues and the need to suppress costs to maintain profitability, leading to the necessity of laying off 30% of their workforce in third quarter in 2023.

The challenges faced by these brand aggregators are rooted from several factors:

Stagnation of Sales

Stagnation of sales are caused by a couple of smaller factors. Most importantly is the habitual shift of people worldwide as they go back to old shopping habits due to physical stores reopening post-pandemic. Additionally, number of competitions also increases especially from new entrants which are drawn by low entry barriers. Lastly, brands are also having problem due to the increased number of knockoffs which manage to take away some of their customers. In combination, these changes have led to little to no growth in sales and reduced profitability for brands under aggregators.

Debt Financing Backfires as Interest Rate Rises

Brand aggregators typically relies on debt financing for its brand acquisition strategy. While this strategy has allowed aggregators to grow rapidly, it now exposes them to vulnerability amidst recent macroeconomic changes, specifically the upswing in interest rates. However, do note that not all brand aggregators rely on this strategy for their growth.

Rising Commission Fees from Key Partners

Almost all brand aggregators leverage technology and key partners to boost their brand sales. Unfortunately, many of them are demanding more share of the pie. E-commerce platforms, merchants, and even logistic partners all ask for a rise in fee. For instance, Amazon commission fee was reported to be as high as 50% in 2022. These changes trimmed the margin from the sales of brands resulting in a decrease in profit for brand aggregators, especially those who rely heavily on such platforms (e.g. Thrasio).

Forced Synergy in Brand Acquisition

Brand aggregators acquire diverse brands with unique operations, cultures, and target customers across different product lines. Forcing integration in pursuit of economies of scale is not always an effective way to develop brands.

D2C

D2C startups have been disrupting traditional retail paradigms by revolutionizing the way brands connect with consumers. These brands, bypassing traditional retail channels and connecting directly with customers, promise a revolution in personalized experiences and streamlined operations.

For brands like Casper, a US-based sleep products e-commerce company, D2C model was a game-changer. By eliminating retailer markups and controlling the narrative, they built a loyal community. Customers resonated with Casper’s transparency, sleek design, and hassle-free delivery, propelling them to a unicorn status with USD 1.1 billion valuation in March 2019 following its USD 100 million Series D before IPO.

However, Casper pursued IPO with initial price range between USD 17 and USD 19. This move resulted in lower company’s valuation compared to its last round, reaching approximately USD 786 million. Ultimately, the company continued with USD 12 per share during IPO, valuing the company at only around USD 575 million.

Just less than two years later in Q3 2021, Casper reported a revenue growth of 26.8% YoY reaching an all-time quarterly high of USD 156.6 million. Despite revenue growth, Casper continued to struggle with profitability, reporting a net loss of USD 25.3 million in Q3 2021, up from USD 15.9 million in Q3 2020.

In November 2021, the company was reported to be acquired by private equity firm Durational Capital Management. Under the terms of the agreement, Casper common stockholders will receive USD 6.90 per share, representing a 94% premium to the closing price on November 12, 2021 (USD 3.56, 69% dip from the IPO price). Following Durational’s acquisition in 2022, Casper diversified beyond mattresses, launching furniture and sleep accessories lines, and start selling through retail partners such as Macy’s and Target.

While these startups have shown promise, there are potential pitfalls that might lead to their downfall. One critical factor is the valuation bubble fueled by exuberant VC funding. Overly optimistic valuations, driven by intense competition among VCs to invest in promising D2C startups, can result in inflated expectations that might not align with the actual market performance, which then can lead to failure in meeting investor expectations, especially regarding revenue growth and profitability.

Private investors are now taking a keen interest in D2C brands in the region, recognizing the potential of a burgeoning middle class and the growing population. The question, however, remains; will the D2C rollercoaster ride in Southeast Asia mirrors the one in the US? Will we see similar patterns of heady valuations, dramatic IPOs, and potential busts? Or will the lessons learned create a more cautious, sustainable approach to profitability in this promising market?

Quick Commerce

Quick commerce represented the next frontier in the evolution of online retail, revolutionizing the way consumers access goods within minutes. Leveraging technology and opening micro-fulfillment centers strategically, quick commerce players endeavor to fulfill orders rapidly, often promising delivery below or within an hour. The appeal goes beyond mere speed; busy professionals value the time saved, urban dwellers appreciate the lack of long commutes, and everyone enjoys the ability to effortlessly restock on forgotten items.

Leading the charge are players like Gorillas, GoPuff and JOKR, opening strategically located dark stores that can fulfill orders in under 15 minutes. Their lightning-fast grocery delivery offerings were sending shockwaves through established food delivery platforms like DoorDash and UberEats. Armed with their existing delivery networks and established user bases, these food delivery titans expand their empires to encompass the grocery market.

Recently, quick commerce startups have faced a challenging landscape as the pandemic's ending prompts people to return to old shopping habits, which has been discussed previously in this article. The joy of personally selecting and purchasing items seems to be resurfacing among consumers. However, the decline in quick commerce is not solely attributed to the pandemic's conclusion. Investors must recognize that the lofty valuations of these startups may have been fueled by irrational exuberance, resulting in inflated prices. Now, as the true value is revealed, these startups are grappling with the repercussions of this market realization:

Instacart took a 40% haircut on their valuation, going down to USD 24 billion from the previous USD 39 billion valuation. As a response, the startup is diversifying its revenue stream by expanding its business line, introducing “Carrot Warehouse” which aims to help grocery retailers to compete with the likes of Amazon by digitalizing and supplying technological needs of grocery stores. In addition, Carrot Warehouse will also provide warehouse and delivery support.

Jiffy ceased delivery operation and rebranded themselves to be a software company, developing a Quick Commerce as a Service (QCaaS) model which allows brands to offer their own quick delivery service but using Jiffy’s ordering system and fulfillment network.

Getir and Gorillas are forced to reduce their workforce as means for a clearer path to profitability.

Final Thoughts

In the ever-evolving landscape of startup trends, the rise and fall of innovative concepts serve as a testament to the dynamic and unpredictable inherent in entrepreneurship. These trends are not merely transient blips on the entrepreneurial radar but reflections of evolving market demands, technological advancements, and shifting consumer behaviors. As we reflect on the patterns of these rising and falling trends, it becomes evident that the success in the startup realm hinges not only on seizing the right opportunity at the right time but also on adaptability, resilience, and ability to pivot in response to changing circumstances. Then how can we know for certain which trends are here to make a lasting impact and which are merely fads?

Disruption

Trends that fundamentally transform industries or solve prevalent problems tend to have a higher chance of making a lasting impact. Disruptive innovations reshape markets, altering consumer behavior and industry norms, demonstrating their potential for longevity. A disruption addresses fundamental human needs in new and efficient ways.

Ride-hailing, for instance, did not just offer another transportation solution, it capitalized on people’s yearning for flexible, on-demand mobility, needs that traditional taxi often fell short of meeting. Ride-hailing services epitomize a disruptive force that revolutionized the transportation industry by addressing the widespread need for accessible, on-demand mobility solutions.

Sustainable business model

While buzzwords and hype can inflate early enthusiasm, a sustainable business model is the bedrock of a trend’s longevity. Can this trend generate sustained revenue? Does it solve a problem at a cost people are willing to pay? Trends built on clear unit economics are here to stay.

Agility

The ability to pivot, evolve, and adapt to new challenges, emerging technologies, or shifts in consumer preferences. The team must exhibit flexibility in adjusting strategies, products, or services in response to market.

Companies like Amazon, with their constant reinvention, exemplify this agility, ensuring their relevance despite shifting landscapes. From online bookstore to e-commerce titan, then cloud computing pioneer, and now dabbling in everything from groceries to healthcare, Amazon constantly sheds its skin and reinvents itself.