Exploring Indonesia's Data Center Boom: Opportunities, Challenges, and the Future of Digital Infrastructure

A data center is a facility designed to house computer systems and related components such as servers, storage units, networking gear, power supplies, and cooling systems. These centers form the backbone of the digital infrastructure, supporting a broad range of services including web hosting, cloud computing, enterprise software, and data storage. As the digital economy continues to expand, data centers are playing an increasingly critical role in enabling connectivity, data processing, and business continuity across sectors.

The growth outlook for data centers is robust, especially in Asia. In Indonesia, the market is projected to grow from USD 2.39 billion in 2024 to USD 3.79 billion by 2030, reflecting a compound annual growth rate (CAGR) of 7.99%. Across the Asia-Pacific region, the market is expected to rise from USD 75.83 billion in 2023 to USD 150.48 billion by 2030, growing at a CAGR of 12%. China, the largest market in APAC, is forecasted to grow from USD 53.05 billion in 2024 to USD 89.67 billion in 2030, representing a CAGR of 9%.

Recent investment commitments signal a robust growth trajectory for Indonesia’s data center market. On May 1, 2024, Microsoft announced a USD 1.7 billion investment plan in AI and cloud infrastructure in the country, marking its largest financial commitment there to date. This investment includes expanding data center capacity and AI skilling programs, catering to the increasing demand for localized cloud services and regulatory trends favoring in-country data residency. Other global players, including Google, Amazon Web Services (AWS), and Tencent Cloud, have also expanded their regional infrastructure. Local operators such as DCI Indonesia, EDGE DC, and NTT Indonesia are continuing to build capacity through both greenfield development and upgrades to existing sites.

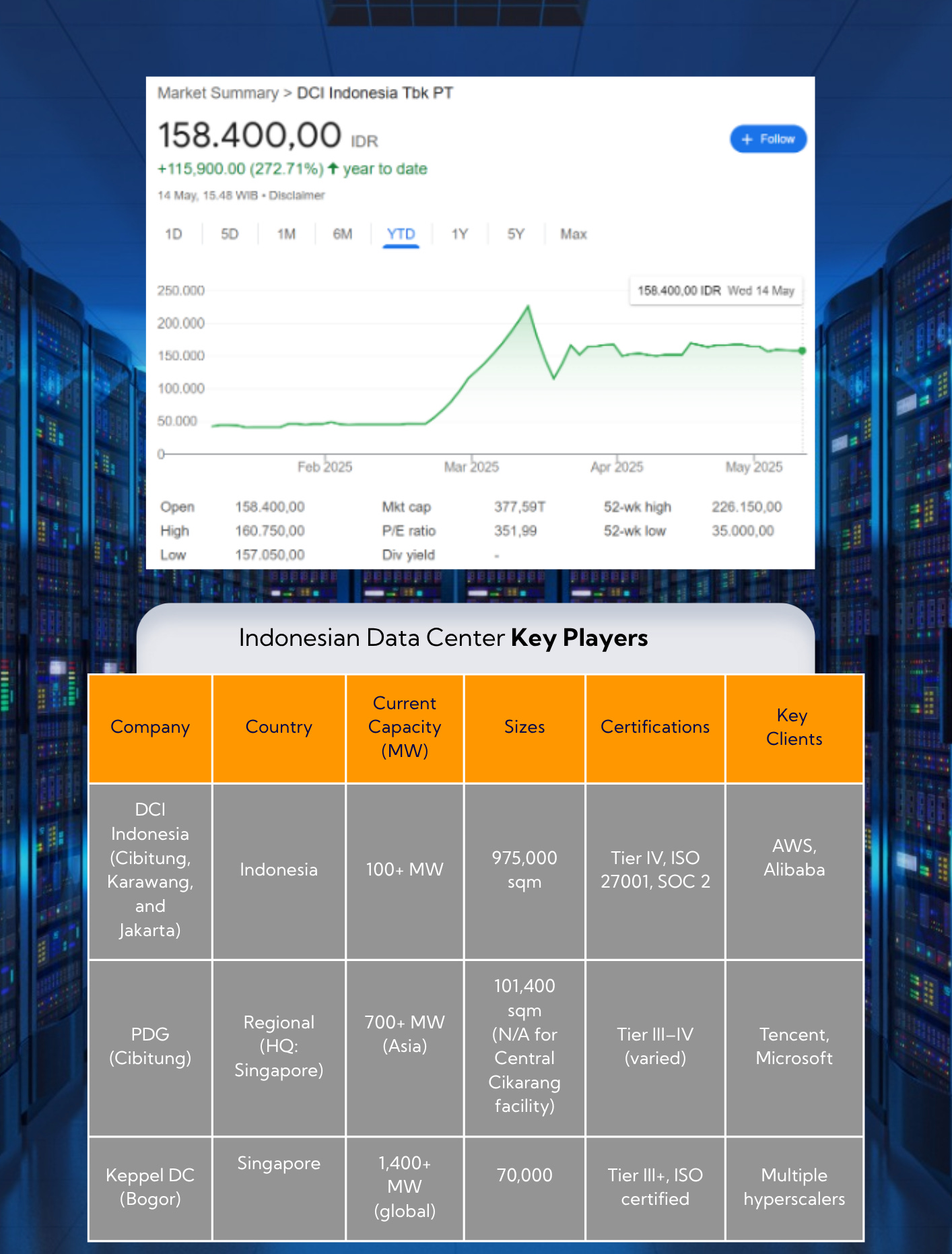

Indonesia’s data center market is transforming, driven by cloud technology, digital banking, e-commerce, and AI workloads. The market is moderately concentrated, with the top five players holding significant shares. Key players include PT DCI Indonesia, Telkomsigma, NTT Communications, XL Axiata through Princeton Digital Group, and GTN Data Center. PT DCI Indonesia stands out as a leader in both scale and certification, making it a critical player in the region's data center landscape.

Indonesia Data Center Industry Landscape

Recent investment commitments signal a robust growth trajectory for Indonesia’s data center market. On May 1, 2024, Microsoft announced a USD 1.7 billion investment plan in AI and cloud infrastructure in the country, marking its largest financial commitment there to date. This investment includes expanding data center capacity and AI skilling programs, catering to the increasing demand for localized cloud services and regulatory trends favoring in-country data residency. Other global players, including Google, Amazon Web Services (AWS), and Tencent Cloud, have also expanded their regional infrastructure. Local operators such as DCI Indonesia, EDGE DC, and NTT Indonesia are continuing to build capacity through both greenfield development and upgrades to existing sites

Indonesia’s data center market is transforming, driven by cloud technology, digital banking, e-commerce, and AI workloads. The market is moderately concentrated, with the top five players holding significant shares. Key players include PT DCI Indonesia, Telkomsigma, NTT Communications, XL Axiata through Princeton Digital Group, and GTN Data Center. PT DCI Indonesia stands out as a leader in both scale and certification, making it a critical player in the region's data center landscape.

PT DCI Indonesia, with over 100 MW IT load capacity (and planning to expand to 300 MW), dominates the market. DCI serves global cloud providers such as AWS, Google Cloud, and Alibaba Cloud and is the only Southeast Asian provider with Tier IV Design and Constructed Facility Certification from the Uptime Institute. PT DCI recorded a revenue of Rp 773.6 billion in Q1 2025, a 118% increase compared to Rp 354.4 billion in Q1 2024, driven by the successful implementation of its business strategy in 2024 and the expanding diversity of its customer ecosystem. The company also expanded capacity by launching new data centers in Karawang and Jakarta—E1 being the first Tier IV data center in the city—serving key sectors like banking and telecom.

Indonesian Data Center Key Players

Market Leaders in Asia

In the broader Asia-Pacific region, several key players are dominating the data center landscape with expansive infrastructure, strategic investments, and global ambitions. Singapore-based ST Telemedia Global Data Centres (STT GDC), for instance, operates more than 95 data centers across 11 regions. In 2024, it secured up to SGD [ET1] [MK2] 2.99 billion (around USD 2.21 billion) in funding from a consortium led by KKR and Singtel to accelerate its global expansion and market strength. Another major Singaporean firm, Keppel Data Centres, is actively scaling to capitalize on the AI boom. The company aims to double its funds under management from SGD 9 billion to SGD 19 billion and expand its gross power capacity from 650 MW to 1.2 GW in the near term.

AirTrunk, another leading operator in the region, was acquired by Blackstone in a landmark USD 24 billion deal. Meanwhile, YTL Power, through its subsidiary YTLDC, is developing the YTL Green Data Center Park in Johor, Malaysia, with a total investment of RM15 billion. The facility will be partially powered by on-site solar energy and forms part of YTL’s collaboration with NVIDIA, aimed at building Malaysia’s fastest supercomputers using NVIDIA’s AI chips under a USD 4.3 billion partnership.

Comparative Analysis: Indonesia vs. Asia-Pacific Market Leaders

While Indonesia’s data center sector is growing rapidly, it still lags behind Asia-Pacific giants in several areas.

Challenges in Building and Operating Data Centers

1. Capital Investment and Infrastructure Requirements

Developing a modern data center requires substantial capital investment due to several factors, including land acquisition, compliance with international certification standards, power availability, and cooling infrastructure. The cost per megawatt (MW) of IT load for constructing a data center in the country typically ranges from USD 7 million to USD 12 million, with higher costs in prime areas like Greater Jakarta or key connectivity hubs. Facilities designed to meet Tier III or Tier IV standards, which demand more complex power and cooling redundancies, will incur additional expenses. For instance, a 20 MW hyperscale-ready facility in Jakarta, incorporating Tier III or IV architecture and sustainable cooling solutions, can cost between USD 150 million and USD 200 million.

Land availability is a key consideration in this equation. Jakarta remains the epicenter of Indonesia's data center activity, with land costs in prime areas like Cikarang and Bekasi reaching IDR 5–10 million per square meter. Hyperscale operators often require large plots of land, ranging from 20,000 to 100,000 square meters, which further increases capital expenditure. The upside of building in these areas is the proximity to enterprise customers, better fiber connectivity, and lower latency. Companies such as DCI Indonesia have secured large land plots in locations like Cibitung’s MM2100 Industrial Park, while others like Princeton Digital Group (PDG) and Telkomsigma are exploring more cost-effective tier-2 cities like Batam and Surabaya. These cities, however, may present challenges related to connectivity and power reliability, making it a trade-off for hyperscale operators seeking to reduce operational costs.

Due to constraints in Singapore, particularly around land availability and power supply, many operators are increasingly turning to alternative locations like Indonesia and Malaysia. These countries offer more favorable expansion opportunities, providing the necessary space and infrastructure for growth that Singapore’s limited resources can no longer fully accommodate.

Power Supply and Reliability

With each data center site demanding between 10 to 50 MW, access to reliable power is critical. Although Indonesia’s grid has improved, power stability and capacity still vary by industrial area. Operators typically collaborate with state utility PLN for dedicated power feeds and backup support. Some industrial zones offer subsidized or industrial electricity tariffs, which reduce opex, but diesel generators are still essential for backup—adding to both capex and ESG concerns.

In India, data centers face challenges in power supply reliability due to grid instability, particularly in regions with fluctuating power availability. While major cities like Bengaluru and Mumbai have more stable grids, operators often rely on diesel generators for backup, raising operational costs and ESG concerns.

3. Cooling and Energy Efficiency

Indonesia’s tropical climate drives up cooling costs. Traditional air-cooled systems are less effective in high humidity and temperatures above 30°C, prompting a shift toward liquid cooling or indirect evaporative systems. Power Usage Effectiveness (PUE) remains a key efficiency metric; global leaders aim for a PUE of 1.3–1.5, while many Indonesian data centers still operate at a less efficient 1.7 or higher. Upgrading to energy-efficient infrastructure could lower operational expenses by 20–30%, but it requires significant upfront investment.

Australia faces similar cooling and energy efficiency challenges as Indonesia, with its diverse climate driving up cooling costs in cities like Sydney and Brisbane. Data centers in these regions often adopt advanced cooling systems, such as liquid cooling, to improve efficiency and meet sustainability goals, despite varying Power Usage Effectiveness (PUE) across the country.

4. Regulation and Compliance

The regulatory environment is tightening. Indonesia’s Personal Data Protection Law (UU PDP), passed in 2022 and phased in over two years, mandates data localization for certain sectors and imposes steep penalties for non-compliance. Operators also need to comply with sector-specific regulations from agencies like OJK, BI, or Kominfo. Achieving certifications like Uptime Institute’s Tier III or ISO 27001 involves design changes, operational audits, and added costs. For new entrants, navigating these requirements can delay market entry by 6–12 months.

The regulatory environment in the Philippines is less stringent compared to countries like Indonesia or China. While there are basic data protection laws, such as the Data Privacy Act of 2012, the country does not have as strict data localization requirements. This allows for more flexibility in data center operations and potentially quicker market entry for operators, though there are still evolving standards to keep an eye on.

5. Talent Scarcity

The scarcity of qualified professionals—particularly data center engineers, facility managers, and compliance officers—is a pressing issue. A 2023 Uptime Institute survey reported that over 50% of Asia-Pacific operators identified staffing shortages as a growth risk. In Indonesia, few educational institutions offer specialized training, leading to a limited talent pipeline. As a result, experienced professionals command high salaries and are frequently poached by multinational operators, contributing to a cycle of brain drain.

Most data center engineers in Indonesia hold degrees in electrical or mechanical engineering or computer science, although diploma holders with practical experience are also in demand. Certifications are key differentiators, with credentials like CDCP (Certified Data Centre Professional), CDCS, CCNA, Network+, and ISO/IEC 27001 commonly required. Engineers must have knowledge of power and cooling systems, server infrastructure, networking, and be adept with DCIM (Data Center Infrastructure Management) tools. Given the 24/7 operational demands, flexibility, attention to detail, and shift availability are crucial. In this maturing market, industry certifications and hands-on training carry increasing weight for employment.

India struggles with a shortage of qualified data center professionals, particularly engineers and compliance officers, due to limited specialized training programs. Many professionals with degrees in engineering or computer science are in high demand, leading to high turnover rates and salary inflation, as multinational operators often poach skilled workers.

")

6. Sustainability, Cost, and Compliance

One of the key challenges in building and operating data centers is meeting Environmental, Social, and Governance (ESG) criteria. As sustainability becomes more important, operators are pressured to adopt energy-efficient technologies and renewable energy sources to reduce their carbon footprint. However, transitioning to these sustainable practices can be costly and complex, particularly in regions where renewable energy infrastructure is still developing. Additionally, complying with ESG regulations, obtaining green certifications like LEED, and investing in energy-efficient systems such as liquid cooling or AI-driven controls require significant upfront investment, which can be a barrier for some operators. Despite these challenges, the demand for ESG-compliant data centers is growing, driven by both hyperscale clients and socially-conscious investors.

Countries like India, Indonesia, and China heavily face ESG challenges in building data centers due to their reliance on fossil fuels, limited renewable energy infrastructure, and high costs for energy-efficient technologies. Navigating evolving regulations and achieving green certifications also present significant hurdles for operators.

Conclusion

Indonesia’s data center landscape is evolving rapidly, fueled by surging digital adoption, regulatory shifts, and the growing presence of global cloud players. While challenges remain—such as energy sustainability, infrastructure reliability, and competition from more mature markets like Singapore—the long-term fundamentals are compelling. With rising demand from hyperscale and enterprise users, and increasing attention from foreign investors, the question now is not whether Indonesia can catch up, but how quickly it can scale to meet global standards and capture its share of Southeast Asia’s digital future.

For investors, the opportunity is clear—but is the ecosystem ready to support sustained, scalable, and differentiated growth?