The Growing Demand for "Salary on Demand"

Another group of FinTech is jumping into the BNPL market - ‘payday loan’ and ‘Earned Wage Access’.

Since the start of the pandemic, there has been an exponential growth in demand for ‘bridge’ short-term loans from cash and credit constrained consumers – at one point as much as 400% in mid-March 2020 and currently at 20% - 30% higher YoY (acc. to Jeanniey Walden, Chief innovation and marketing officer at DailyPay).

Other than BNPL providers that collaborate with merchants to allow for purchase of specific products, another group of FinTech jumping into this market is ‘payday loan’ and ‘Earned Wage Access’ providers—both typically targeted towards low- and moderate-income households with lack of access to cashflow or traditional credit methods.

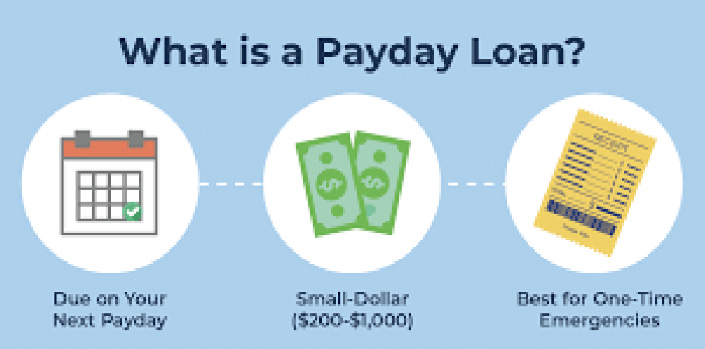

What are ‘Payday Loans’?

Payday Loans, as originally conceived, are short-term loans designed to prevent borrowers from having to resort to (what is perceived as) ‘high-interest’ loans such as credit cards and overdrafts. This has also been referred to as ‘payday advance.’ Liquidity shortage and sudden unexpected costs are the issue that this type of financing hopes to resolve. Originally this type of financing is not intended to be recur-ring or continuous, rather only in the event of emergencies.

Generally, they can be anywhere between $50 to $1000 with terms of two weeks all the way up to six months. Different providers charge differently – some will charge interest income, while others charge a flat-fee per transaction. This type of loan is not automatically avail-able, nor is it linked to your performance, payroll, or time management software.

How does it differ from ‘Earned Wage Access’?

An alternative to payday loans are Earned Wage Access services that enables employees to take out only salaries that they have worked for but are yet to be disbursed. These loans are provided either directly to consumers or through employers but rely heavily on access to the company’s payroll system. They generally have simpler fee structures, lower fees, and shorter payback periods.

Although, when not integrated with employer payroll systems, consumers may need to prove that they are getting paid regularly. Some providers use technology to track or anticipate when incoming payments will hit a customer's bank account.

Who provides these loans?

Employers originally provided such loans as a type of ‘advance,’ later deducting the borrowed amount from the end of month pay-check. Amongst smaller ‘mom and pop’ type businesses this type of practice is in fact common.

Today many private companies, such as Speedy Cash and Advance America, offer these unsecured loans with their own underwriting criteria, typically conducting verification of employment or income via bank statements or pay stubs. In order to reduce turnover and boost morale, some companies have even began partnering with these loan providers to provide their employees access to salary advance. In fact, there has been a particularly strong demand from the employer side amongst the retail, hospitality and telemarketing industries as it is relatively simpler to track the hours worked ‘wages’ earned.

In the 2010s, alongside the rise of P2P lending, startups began venturing in the payday loan space – some of these successful players include:

DAILYPAY (USA, 2015)

Considered the leading FinTech for earned income software with over 500corporate clients, DailyPay specializes in the employer-employee relation-ship by offering salary advances with a $2-3 flat fee. Their clients include McDonald's, TacoBell, Six Flags, Berkshire Hathaway and Burger King. Even large payroll service providers, such as ADP LLC, are working with DailyPay to offer these services to all their client.

Latest Funding: $50M Series C

Notable Investors: RPM Ventures, FinVenture Capita

PAYACTIV

Officially classified as a ‘Public BenefitCorporation’ that focuses on helping lower income/freelance consumers, PayActiv allows employees to take out a portion of their paycheck at no cost if they receive their wages through the PayActiv Visa debit card. They levy a $1 fee if customers choose to receive their wages in a different account, and it charges $1.99 for instant transfers. They serve over 2,000 businesses including Walmart and Wendy’s but caters to SME with less than 100 employees as well.

Latest Funding: $100M Series C

Notable Investors: Eldridge, Generation Partners and Ziegler LinkAge Fund II

DAVE

Dave allows consumers to take out up to$75 prior to payday (up to $100 if they sign on to the free Dave bank account), and customers can choose to add on optional tips. For an additional $1 per month, Dave customers also have access to automated personal finance and budgeting tools, and access to Side Hustle, a job-finding platform.

Latest Funding: $50M Series B

Notable Investors: Victory Park Capital, Norwest Venture Partners

SQUARE (USA, 2020*)

To accompany its payroll service, Square also leverages its P2P Cash App system for the distribution of earned-wage salaries on demand. This feature, launched September 2020, allows employees can transfer up to $200 of their earned wages to the Cash App for no fees or transfer the money to a linked card for a 1% fee capped at $2. Square made its debut on the NYSE onNovember 2015 with a valuation of $2.9B.

*2020 refers to the launch of the payday loan product

HASTEE (UK, 2017)

Hastee launched UK’s first earnings-on-demand app in 2017 and later the world’s first earning-on-demand debit card in June 2020. The company enables workers to withdraw up to 50% of their daily salary on the day they earn it.

Latest Funding: $20M Series A

Notable Investors: IDC Ventures, Umbra Capital Partners

DOREMING (JAPAN, 2015)

Aside from providing payroll services, Doreming allows workers to see how much they have earned each day and make purchases using that money, simply by scanning QR codes at shops. Employers then pay the stores, electronically. Through partnerships with local conglomerates, they have established operations in various countries, including the USA, India, and Saudi Arabia.

Latest Funding: Undisclosed

Notable Investors: Level 39

What are the risks and how can we mitigate them?

Although marketed to consumers as a cheaper and more flexible form of financing, several providers in the US are currently under the scrutiny of US state regulators for using quasi-transaction-based mechanisms that have at times amounted to a 400%+ annual percentage rate for a two-week loan. Due to these high interest rates, plenty of lenders are unable to pay back their loans and eventually found themselves facing bankruptcy. A StepChange study found that only 64% of payday loans issued in in the United Kingdom from 2012 were repaid in full, either early or on time.

Regulators are actively restricting the practice of these short-term loan services. Most developed countries apply a limit on the loan amount, the fees, and/or the interest rates payday loan companies can charge. Some states in the US, including New York and DC, even prohibit high cost payday lending. The rise of the Earned Wage Access model also aims to lower the risk of default, as their borrowers would eventually receive their salary payments. That said, many borrowers find themselves in a cycle where they are continuously dependent on these short-term loans and spending a sizable sum of money on fees/interest rates.

While the number of payday loans and Earned Wage Access providers in Asia are still very limited, we expect to see a growth in this industry in Indonesia and surrounding Southeast Asian countries. So now the question is whether this new and improved business model could be the solution to predatory lending, bettering the lives of its borrowers? Or are they really contributing to the normalization of debt and the increase in the number of ‘lifestyle borrowers’ spending their monies on frivolous items—when in fact they should be learning how to manage their finances better with current means.